CBSE exams 2019: Class 12 Accountancy sample paper

21 January 2019

CBSE has released the date sheet of class 12 exams, according to which, exams will begin from February 15. The board has scheduled the Accountancy paper on February 27, 2019. Here is the sample paper for students:

Part A

(Accounting for Partnership Firms and Companies)

What is compulsory dissolution of partnership firm? A, B and C were partners in a firm sharing profits in the ratio of 3:2:1. C was guaranteed a profit of 20,000. During the year the firm earned a profit of 84,000. Calculate the net amount of Profit / Loss transferred to the capital accounts of A and B.

OR

A, B and C were partners in a firm sharing profits in the ratio of 3:2:1. A gave guarantee to C that C will get minimum profit of 20,000. During the year the firm earned a profit of 84,000. Calculate the net amount of Profit / Loss transferred to the capital accounts of A and B.

H, P and S were partners in a firm sharing profits in the ratio of 4:3:3. On August 1, 2017 P died. His 20% share was acquired by H and remaining by S. Calculate the new profit sharing ratio.

OR

How is dissolution of partnership different from dissolution of partnership firm?

Name the account which shows the classified summary of transactions of cash book in a not-for-profit organization.

What is Private placement of shares?

OR

Give one provision of Section 52 (2) of Companies Act, 2013.

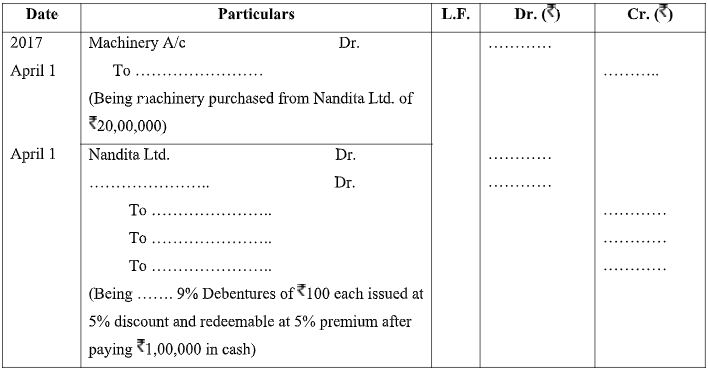

Mehta Limited obtained a loan of 1,00,000 from State Bank of India @ 7% interest. The company issued 1,500 9% debentures of 100 each in favor of State Bank of India as collateral security. Pass necessary Journal entries for the above transactions:

When company decided not to record the issue of 9% Debentures as collateral security.

When company decided to record the issue of 9% Debentures as collateral security.

Mukesh, Praveen and Akhilesh were partners in a firm. They share the profit in the ratio of 2:2:1. With effect from 1st April, 2017 they decided to share future profit in the ratio of 1:1:1. On this date, there was balance of Profit and Loss Account 15,000. Partners decided to not to alter the values. Pass the single adjusting entry for the above.

Suzuki Limited is registered with an Authorized capital of 200 Crores divided into equity shares of 100 each. The Subscribed and Called up capital of the company is 10,00,00,000. The company decided to help the unemployed youth of the naxal affected areas of Andhra Pradesh, Chhattisgarh and Odisha by opening 100 ‘Skill Development Centers. The company also decided to provide free medical services to the villagers of these states by starting mobile dispensaries. To meet the capital expenditure of these activities the company issued 1,00,000 equity shares. These shares were fully subscribed and paid.

Present the share capital of the company in its Balance Sheet.

OR

Complete the following entries:

From the following information of a club show the amounts of Match Expenses and Match fund in the Financial Statements of the club for the year ended on 31st March, 2018.

Details

Match expenses (paid during the year 2017-18) 30,000

Donation for Match Fund (Received during the year 17-18) 9,000

Proceeds from the sale of match tickets (Received during the year 17-18) 3,000 3

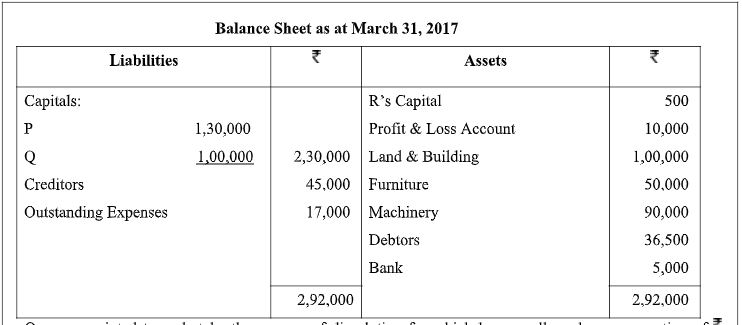

P, Q and R were partners in a firm sharing profits in the ratio of 2:2:1. On September 30, 2017, their firm was dissolved. On the date of dissolution, the Balance Sheet of the firm was as follows:

Q was appointed to undertake the process of dissolution for which he was allowed a remuneration of 5,000. Q agreed to bear the dissolution expenses. Assets realized as follows:

The Land & Building was sold through a property dealer at a price of 110% of the book value. A Commission of 1% on the selling price of Land & Building was paid to the property dealer.

Furniture was sold at 25% of book value.

Machinery was sold as scrap for 9,000.

Creditors were payable on an average of 3 months from the date of dissolution. On discharging the Creditors on the date of dissolution, they allowed a discount of 5%.

Pass necessary Journal entries for dissolution in the books of the firm assume that the entries of assets and liabilities have already been passed.

X, Y and Z were partners sharing profits in the ratio of 2:2:1. The firm closes its books on March 31 every year. On June 30, 2017, Z died. The following information is provided on Z’s death:

Balance in his capital account in the beginning of the year was 6,50,000.

He withdrew 60,000 on May 15, 2017 for his personal use.

On the date of death of a partner the partnership deed provided for the following:

Interest on capital @ 10 % per annum.

Interest on drawings @ 12 % per annum.

His share in the profit of the firm till the date of death, to be calculated on the basis of the rate of Net Profit on Sales of the previous year, which was 25 %. The Sales of the firm till June 30, 2017 were 6,00,000.

Prepare Z’s Capital Account on his death to be presented to his executors.

L, M and N are partners in a firm sharing profits & losses in the ratio of 2:3:5. On April 1, 2016 their fixed capitals were 2,00,000, 3,00,000 and 4,00,000 respectively. Their partnership deed provided for the following:

Interest on capital @ 9% per annum.

Interest on Drawings @ 12% per annum.

Interest on partners’ loan @ 12% per annum.

On July 1, 2016, L brought 1,00,000 as additional capital and N withdrew 1,00,000 from his capital. During the year L, M and N withdrew 12,000, 18,000 and 24,000 respectively for their personal use. On January 1, 2017 the firm obtained a Loan of 1,50,000 from M. The Net profit of the firm for the year ended March 31, 2017 after charging interest on M’s Loan was 85,000.

Prepare Profit & Loss Appropriation Account and Partners Capital Account. From the following information supplied by the accountant of Lions Club for the year ended 31st March, 2018, prepare Income and Expenditure Account.

Additional Information:

The club has 400 members each paying an annual subscription of 50.

Stock of Stationery on 31.3.2017 780 and on 31.3.2018 860.

On 1st April 2017, Premises were 16,000. Depreciation on Premises and Furniture to be charged @5% and 10% p.a. respectively. Solve the following:

A, B, C and D are partners sharing profits and losses in the ratio of 3:1:2:1. Their fixed capital on 31.3.2018 were 60,000, 90,000, 1,20,000, and 90,000 respectively. After preparing the final accounts for the year ended 31.3.2018 it was discovered that interest on drawings amounting to 2,000, 2,500, 1,500 and 1,000 respectively was not charged. Pass the necessary adjustment entry showing your workings clearly.

A firm’s average profits are 1,80,000. Capital invested in the business is 5,00,000 and the normal rate of return is 20%. Calculate the value of goodwill of the firm by capitalization of Average Profit.

ZX Limited invited applications for issuing 5,00,000 Equity shares of 10 each payable at a premium of 10 each payable with Final call. Amount per share was payable as follows:

Applications for 8,00,000 shares were received. Applications for 50,000 shares were rejected and the application money was refunded. Allotment was made to the remaining applicants as follows:

Excess application money received with applications was adjusted towards sums due on allotment. Balance, if any was adjusted towards future calls. Govind, a shareholder belonging to category A, to whom 1,500 shares were allotted paid his entire share money with allotment. Manohar belonging to category B had applied for 11,000 shares failed to pay ‘Second & Final Call money’. Manohar’s shares were forfeited after the final call. The for feited shares were reissued at 15 per share as fully paid.

Pass necessary Journal entries for the above transactions in the books of ZX Limited.

OR

Vivek Ltd. invited application for 30,000 shares of 100 each at a premium of 20 per share payable as follows:

On application 40 (including 10 premium)

On allotment 30 (including 10 premium)

On first call 30

On second and final call 20

Application were received for 40,000 shares and pro-rata allotment was made on the application for 35,000 shares. Excess application money is to be utilized towards allotment.

Rohan to whom 600 shares allotted failed to pay the allotment money and his shares were forfeited after allotment.

Mohit who applied for 210 shares failed to pay first call and his shares were forfeited after first call. Second and final call was not made. Out of Rohan’s forfeited shares, 500 shares were reissued at 80 paid up for 60 per share. Record journal entries in the books of Vivek Ltd.

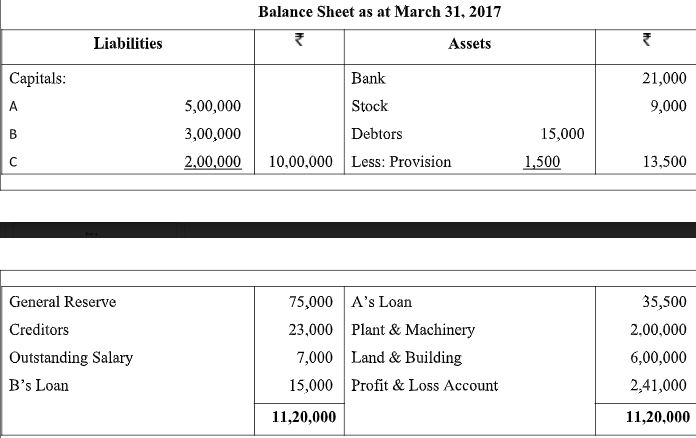

A, B & C were partners in a firm sharing profits & losses in proportion to their fixed capitals. Their Balance Sheet as at March 31, 2017 was as follows:

On the date of above Balance Sheet, C retired from the firm on the following terms:

Goodwill of the firm will be valued at two years purchase of the Average Profits of last three years. The Profits for the year ended March 31, 2015 & March 31, 2016 were 4,00,000 & 3,00,000 respectively.

Provision for Bad Debts will be maintained at 5% of the Debtors.

Land & Building will be appreciated by 90,000 and Plant & Machinery Will be reduced to 1,80,000.

A agreed to repay his Loan.

The loan repaid by A was to be utilized to pay C. The balance of the amount payable to C was transferred to his Loan Account bearing interest @ 12% per annum. Prepare Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of the reconstituted firm.

OR

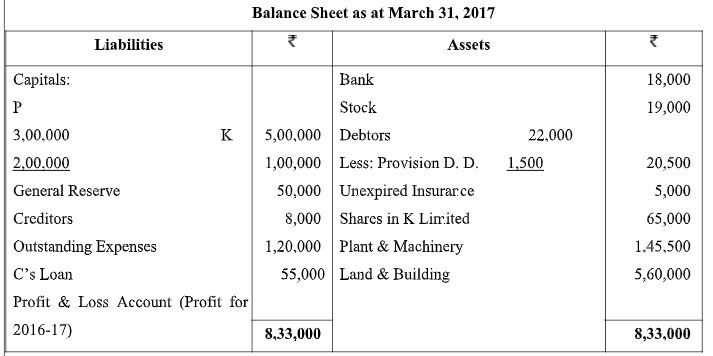

P & K were partners in a firm. On March 31, 2017 their Balance Sheet was as follows:

Balance Sheet as at March 31, 2017

On April 1, 2017, they decided to admit C as a new partner for 1/4th share in profits on the following terms:

C’s Loan will be converted into his capital.

C will bring his share of goodwill premium in Cash. Goodwill of the firm will be calculated on the basis of Average Profits of previous three years. Profits for the year ended March 31, 2015 and March 31, 2016 were 65,000 and 1,00,000 respectively.

10% depreciation will be charged on Plant & Machinery and Land & Building will be appreciated by 5%.

Capitals of P & K will be adjusted on the basis C’s capital. Actual cash will be bought in or paid off as the case may be.

Pass necessary Journal entries on C’s admission.

Part B

(Analysis of Financial Statements)

Give any two examples of cash inflows from operating activities other than cash receipts from sale of goods & rendering of services.

Verma Limited is Share Broker Company. Sharma Limited is engaged in manufacturing of packaged food. Verma Limited purchased 5,000 equity shares of 100 each of Rashmi Limited. Sharma Limited also purchased 10,000 equity shares of 100 each of Rashmi Limited. For the purpose of preparing their respective Cash Flow Statements, under which category of activities the purchase of shares will be classified by Verma Limited and Sharma Limited?

K Limited is a computer hardware manufacturing company. While preparing its accounting records it takes into consideration the various accounting principles and maintains transparency. At the end of the accounting year, the company follows the ‘Companies Act and Rules, 2013’ for the preparation of its Financial Statements. It also prepares its Income Statement and Balance Sheet as per the format provided in Schedule III to the Act. Its Financial Statements depict its fair & true financial position. For the financial year ending March 31, 2017, the accountant of the company is not certain about the presentation of the following items under relevant Major Heads & Sub Heads, if any, in its Balance Sheet:

Securities Premium Reserve

Calls in Advance

Stores & Spares

Mastheads

Advice the accountant of the company under which Major Heads and Sub Heads, if any, he should present the above items in the Balance Sheet of the company. For the year ended March 31, 2017, Net Profit after tax of X Limited was 6,00,000. The company has 40,00,000, 12% Debentures of 100 each. Calculate Interest Coverage Ratio assuming 40% tax rate. State its significance also.

OR

A company had a Liquid Ratio of 1 and Current Ratio of 2 and Inventory turnover Ratio of 5 times. It had a total Current Assets of 4,00,000 in the year 2016-17. Find out the revenue from operation if goods are sold at a profit of 25% on cost.

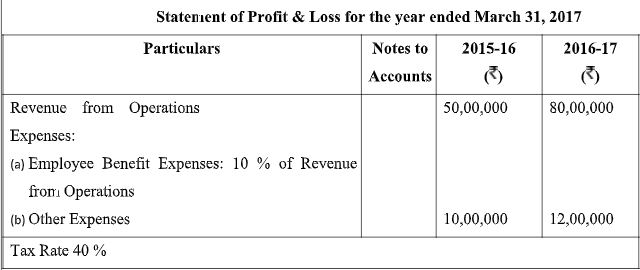

Following is the Statement of Profit & Loss of X L Limited for the year ended March 31, 2017

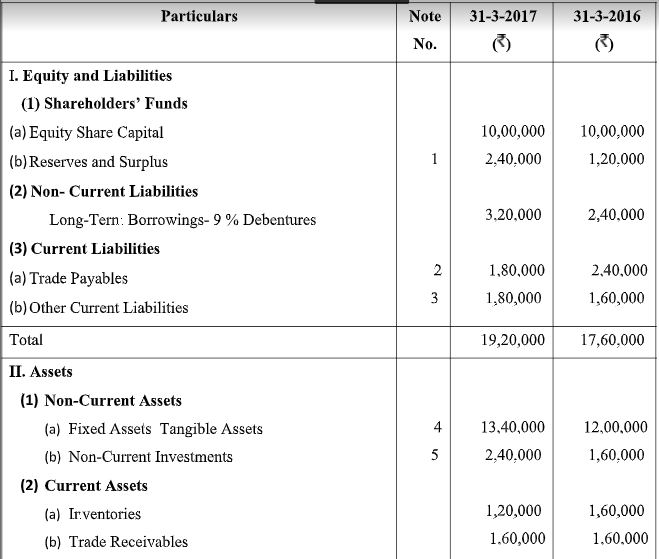

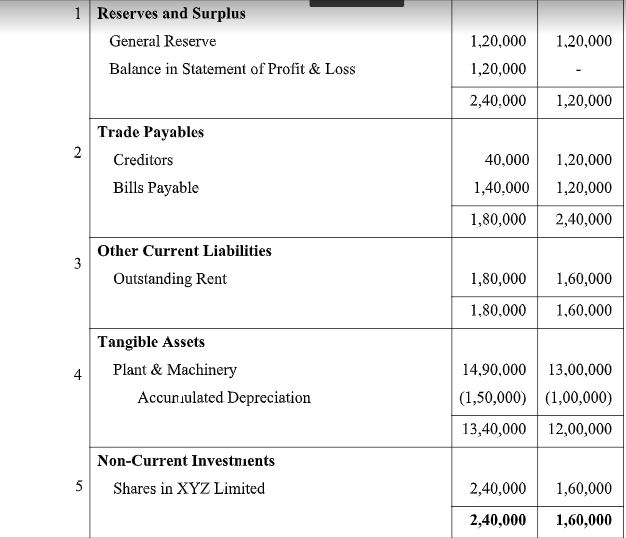

From the following Balance Sheet of Ajanta Limited as on March 31, 2017, prepare a Cash Flow Statement:

Additional Information:

During the year 2016-17, a machinery costing 50,000 and accumulated depreciation thereon 15,000 was sold for 32,000.

9 % Debentures 80,000 were issued on April 1, 2016.

News Soource (Indian Express)

Want help with admissions?

Leave us your details and we will contact youApplications for Admissions are open

K.R. Mangalam University, Gurgaon

Gurgaon

Alliance University

Bangalore

Woxsen University

Hyderabad

Bennett University, Greater Noida

Greater Noida

RV University

Bangalore

Desh Bhagat University

Fatehgarh Sahib

Genesis Institute Of Dental Sciences and Research

Firozpur

Guru Kashi University

Bathinda

IILM University, Gurugram

Gurgaon

IILM University, Greater Noida

Greater Noida

Institute of Technology & Science, ITS Ghaziabad

Ghaziabad

Manav Rachna Dental College

Faridabad

Universal Business School

Mumbai

Chanakya University

Bangalore

I.T.S Engineering College

Greater Noida

International School of Management Excellence, Bangalore

Bangalore

Saraswati Group of Colleges, Mohali

Mohali

GD Goenka University, Gurgaon

Gurgaon

Geeta University

Panipat

Anant National University

Ahmedabad

Mangalmay Group of Institutions

Greater Noida

Lovely Professional University

Jalandhar

Karnavati University

Gandhinagar

Atria University

Bangalore

National Dental College & Hospital

Mohali

Gokul Global University

Siddhpur

Guru Nanak Ayurvedic Medical College & Hospital

Guru Nanak Ayruvedic Medical College & Research Institute

Ludhiana

Firebird Institute of Research in Management

Coimbatore

Manav Rachna International Institute Of Research And Studies

Faridabad